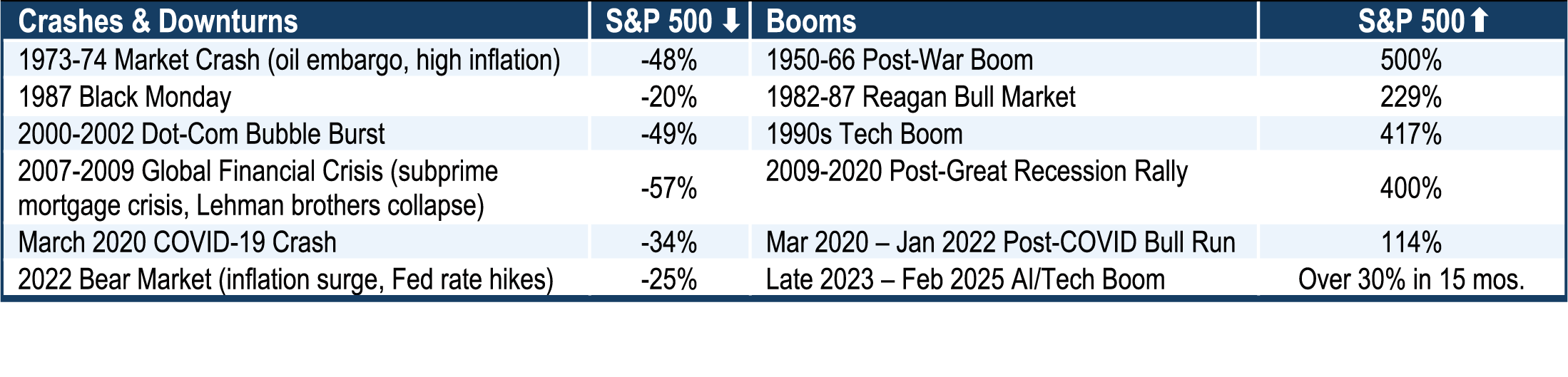

Markets in Historical Context

The S&P 500 market index recently reached an all-time closing high of 6,144.15 on February 19. Then on April 7 the S&P 500 closed at 5,062.25, marking a 17.6% decline from its February peak. Markets have always moved up and down, with those movements measured as volatility. For context, here are some of the most significant downturns and booms since 1950 reflected in the S&P 500.

“Time in the Market” vs “Timing the Market”

Most of us have heard the age-old advice for investing: “Buy low, sell high.” While this adage may be accurate in its simplicity, it can be a mistake for most of us to pursue it as our big aim.

Let’s look at the root of the concept – timing. “Timing” encourages the mindset of trying to guess when a particular type of investment is at a “low” when you are trying to buy-in/purchase. And it creates a sense of alertness to watch for the “right time” to sell. Though this is correct mathematically and logically, it can feed emotional and knee-jerk reactions, and cause anxieties and concerns.

Trying to time the market causes us to watch and analyze our investments more often than is helpful. Keeping in touch with what is happening in the markets is good, but for most of us, it’s better to review our retirement investments periodically, once or twice a year, with a three to five-year or longer focus, and then leave them alone. Whether you are retiring next year, in five years, or in twenty-five years, a good investment plan strategy allows us the time we need to keep money invested for growth, knowing that none of us can perfectly time the market. Many of the best days in the market happen shortly after the worst days. If you missed the ten best days in the U.S. stock market over the last twenty years, your total return would be cut nearly in half, and missing the thirty best days could end up with no return or even a loss.

Maximizing Investments and Thinking Long-Term

As you can see from historic examples, market drops occur from time to time and will continue to do so. There will be more in the future; we don’t know when, or how long they will last. Rather than mainly focusing on the current market value of our long-term investments, it can be beneficial to focus on the number of shares we own while we are investing. During our working years, it is good to invest all we can (i.e. acquiring as many shares as we can) to give our investments time and opportunity to grow. When you buy “shares” of an investment, the value of your account depends on the number of shares you own times the value of those shares on that day. In the short term, the values will go up and down, but over the long-term, history has shown us that patience in steady investing will best serve us with long-term growth.

With a long-term perspective, during a market downturn we can have the satisfaction of two things:

(1) We haven’t lost any of the shares we previously purchased (and)

(2) The new money that is going in is buying more of those shares at a lower price!

Once the price per share recovers, we’ll not only have the same value as before, but we’ll be money ahead for all those shares we bought “on sale.” Dollar-cost averaging is a helpful strategy of investing money in equal portions, at regular intervals, regardless of the ups or downs in the market. This investment strategy can help manage risk and makes us more likely to stay in the market focused on our long-term goals. In a retirement plan, we can do this through regular “employer” and “employee” contributions and their corresponding investments, maximizing our opportunity to grow our number of shares over time.

In retirement, and as we near retirement, we can also protect ourselves by allocating our money to different types of investments not invested in stock funds, and therefore not subject to the same levels of market volatility and valuation fluctuation. This keeps the money we need for the short-term, or even the long-term, from experiencing the same volatility in valuations.

Actions to Consider

Review your asset allocation – Align your investments with your long- and short-term goals.

Review current employee contributions – Ensure you are contributing at the level that fits your plan for retirement and takes advantage of dollar-cost averaging.

Contact Us

FCMM is here to serve you. As you serve the Lord, faithfully steward resources and trust Him as provider, we are here to help give you confidence and support in planning for retirement. If you would like to discuss maximizing your contributions and investments, investment allocation and strategy, or anything else we can help you with, please call us at (800) 995-5357 or reach out to us via email at fcmm@fcmmbenefits.org.